A pencil can be a great learning tool.

I’m not referring to the obvious fact that you can write and take notes with one.

Many years ago, I went through a finance class where the teacher used a pencil to help me understand the inverse relationship between bond prices and interest rates. His explanation went like this:

Hold a pencil horizontally in front of you. The left end of the pencil represents the price, or value, of the bond, and the right end of the pencil represents the interest rate. To illustrate, think of the picture below as a pencil you are holding.

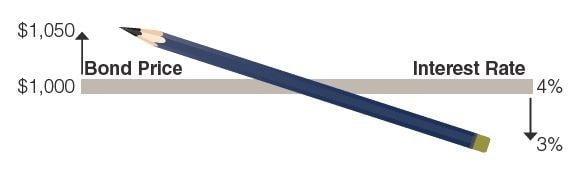

Now we’ll add some numbers. At issuance, the bond price starts at the par, or face value, and it has a stated interest rate that is generally fixed over the life of the bond. Below is an example of a five-year, $1,000 bond, issued with a stated interest rate of 4%.

The bond issuer pays interest payments of $40 each year until the bond matures in five years, and you receive your $1,000 back. Below I added the current bond price and interest rate to the illustration.

What if interest rates rise?

When interest rates rise, it causes bond prices to fall, because investors can now purchase a similar quality and duration bond but with a higher coupon rate. Using the pencil for a visual representation helps demonstrate the point. When you raise the interest rate end of your pencil, it lowers the bond price side of the pencil.

In this case, if rates were to rise by 1% and you tried to sell your 4% bond, you would find out that no one would be willing to pay the full $1,000 par value, because they could buy a similar bond for $1,000 with the higher current interest rate of 5%. You would have to sell your current bond at a price below $1,000 to make it worthwhile for the buyer.

What if interest rates fall?

Inversely, when interest rates go down, bond prices go up. To see this, lower the interest rate side of your pencil and see how the bond price side rises.

Using our original five-year 4% bond as an example, if market interest rates move down 1%, your bond is now worth more, because similar bonds available for purchase are only paying an interest rate of 3%. If you decided to sell the bond, you would require the buyer to pay a price above the $1,000 to make it worthwhile.

Understanding the relationship between interest rates and bond prices could make it easier to become overly concerned about day-to-day price movements. However, it’s important to remember that those movements don’t really amount to much if you hold a bond to its maturity.

The price movements are just a reflection of what you could get for your bond if you sold it at that time. If you don’t sell, the price of your bond will gradually move closer to its par value as it gets nearer to its maturity date. At maturity, barring default, you get your principal back.

If you invest in fixed income using mutual funds, you don’t have to worry about individual bonds and their maturity dates. A mutual fund holds a large basket of bonds, each with its own interest rate and maturity date. The fund will have a yield and duration based on its underlying holdings, and the price of the fund will fluctuate based on the daily prices of those holdings. However, as with an individual bond, the price movements are a reflection of what you could get for a share of the mutual fund if you sold it at that time.

Another thing to keep in mind is that not all bonds are created equal. Depending on the credit quality of the issuer and the term or length of time to maturity, bonds react differently to interest rate movements. To learn more about these two characteristics, term and credit, visit the blog on our website entitled What Kind of Bonds Should be in My Portfolio?

Sitting in my finance class years ago, I never thought of someday writing an article about what I was learning from a pencil. I love finding easier ways to understand complicated things. Hopefully, these illustrations and examples help you better understand the inverse relationship between interest rates and bond prices.

PLEASE NOTE LIMITATIONS: Please see Important Disclosure Information and the limitations of any ranking/recognitions, at www.fostergrp.com/info-disclosure/. A copy of our current written disclosure statement as set forth on Part 2A of Form ADV is available at www.adviserinfo.sec.gov.